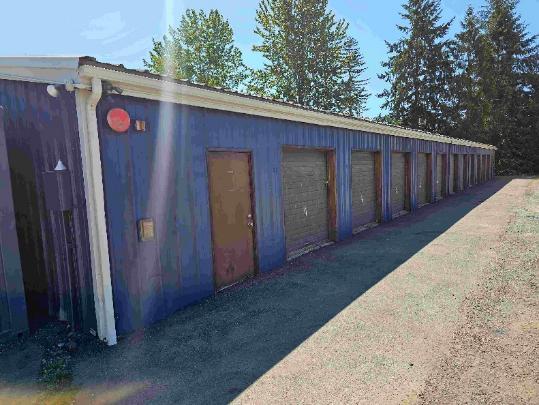

A developer on Vashon Island, Washington faced a wall of rejections when seeking financing for a $2.15 million mixed-use project combining self-storage with retail space. With only 11,000 residents on an island accessible only by ferry, traditional lenders couldn’t find comparable properties to justify their underwriting models.

The project embodied everything conventional lenders avoid: an unstabilized mixed-use property in a micro-market with no direct comparables, structured as a cash-out refinance rather than acquisition or development financing. The borrower had assembled 15,000 square feet of climate-controlled self-storage units alongside 3,500 square feet of retail space, but occupancy sat at just 60% with retail tenancy at 40%.

Traditional portfolio lenders walked away immediately. The island location meant no comparable sales data within a 50-mile radius. The mixed-use nature complicated standard self-storage underwriting models. And the cash-out structure on an unstabilized property triggered additional risk flags across every institutional lending desk the borrower approached.

This scenario illustrates a broader challenge facing small-market commercial real estate: properties that make economic sense but don’t fit standardized lending criteria. When you combine specialty asset classes with unique geographic constraints, finding appropriate financing requires lenders willing to dig deeper than surface-level metrics.

Self Storage Market Dynamics Drive Small Market Opportunities

Self storage financing in small markets has become increasingly viable as demand patterns shift beyond major metropolitan areas. According to the Self Storage Association’s 2024 industry report, occupancy rates in markets under 50,000 people averaged 87.2% compared to 85.1% in major metros, suggesting stronger fundamentals in smaller communities. Self Storage Association

Small market dynamics often work in favor of self-storage operators. Yardi Matrix data from Q4 2024 shows that self-storage facilities in markets with populations between 10,000-50,000 people achieved average rental rates of $1.47 per square foot annually, while new supply additions remained 40% below the national average. Yardi Matrix

Mixed-use self-storage properties present additional complexity but can generate stronger returns through diversified income streams. CoStar research indicates that mixed-use self-storage properties with complementary retail achieved 12% higher net operating income per square foot compared to single-use facilities in markets under 25,000 people, though financing options remain limited. CoStar Group

The financing gap becomes most pronounced in micro-markets where traditional lenders struggle with comparables. CBRE’s 2024 capital markets report noted that 73% of self storage transactions under $5 million in markets with populations below 15,000 required non-traditional financing sources due to limited comparable sales data. CBRE

How QuadBlock Structured the Vashon Island Deal

The Vashon Island project required a lender willing to look beyond traditional metrics. QuadBlock’s underwriting team focused on three key factors: the island’s demographic stability, the property’s strategic location near the ferry terminal, and the borrower’s operational track record with similar assets in the Pacific Northwest.

Rather than relying on direct comparables, QuadBlock analyzed rental rates across similar island communities in Washington and Oregon, adjusting for population density and seasonal factors. The team validated demand by examining Vashon’s housing characteristics: 68% of island residents live in homes built before 1980, creating above-average storage needs, while the absence of competing facilities within a 45-minute drive supported pricing power.

The mixed-use component actually strengthened the deal structure. The retail space, designed for island-appropriate tenants like marine supply and local services, provided immediate income diversification. QuadBlock structured a 24-month bridge loan at 75% LTV, allowing the borrower to stabilize occupancy while pursuing permanent financing.

Where other lenders saw four strikes against the deal, QuadBlock identified sustainable cash flow backed by limited competition and demographic stability. The property generated sufficient debt service coverage at current occupancy levels, with clear upside as both storage and retail components reached stabilized occupancy.

Self storage financing for small market deals often requires this type of creative underwriting. Traditional models break down when comparable sales data doesn’t exist, but economic fundamentals can support solid lending decisions when analyzed properly.

What This Means for Borrowers

Small market mixed-use properties require lenders who understand local dynamics rather than relying solely on automated underwriting systems. The key for borrowers is presenting a comprehensive market analysis that addresses the unique characteristics driving demand in their specific location.

When pursuing self storage financing in small markets, focus on demographic factors that support storage demand: housing age, seasonal population fluctuations, local business characteristics, and proximity to population centers. Document the competitive landscape thoroughly, including drive-time analysis to alternative facilities. Most importantly, demonstrate your operational experience with similar assets and markets, as lenders will weight management capability heavily when traditional comparables aren’t available.

Have a Deal That Doesn’t Fit the Box?

QuadBlock Capital specializes in financing $5M-$30M commercial real estate deals that require a closer look. Bridge loans, permanent financing, and construction loans with 24-48 hour LOIs.

Sources & References

- Self Storage Association — occupancy rates by market size

- Yardi Matrix — small market rental rates and supply data

- CoStar Group — mixed-use self-storage performance metrics

- CBRE — small market transaction financing patterns